I have to pay tax on my scholarships — and you might, too

Navigating the world of college admissions as a first-generation, low-income kid was already a large feat in itself. For much of my high-school career, in-state seemed to be the only feasible option—both for me, and for my family. Enter the world of QuestBridge, which shook my entire outlook on my college aspirations during my junior year. Being a College Prep Scholar, then applying to the National College Match, it seemed as simple as what it said on the tin:

"Finalists who match are admitted to a college partner with a full four-year scholarship, worth over $325,000."

What they don't say (and in fact, no one at all really cared to mention... anywhere) is that much of that scholarship is taxable. And that means that a demographic of students already possibly from families with lackluster standings in financial literacy have a whole new, confusing, and mystical realm to manage: their likely newfound tax burden, and a new lump of money to pay up to Uncle Sam for students who depend on every dollar in their scholarship to make school accessible in the first place—to make QuestBridge's "a top college is possible" catchphrase prove true.

This sudden realization was the basis for me to create this wonderful place I proudly call my "array of hyperfixated thoughts"; when I stumble into something I bear responsibility for, I will not and honestly cannot stop researching and devouring the entirety of the interweb until I come to a sound conclusion. So, follow me through this journey through tax law (as I've already had to become all too acquainted with for my family) and all the wonderful quirks that come with it—both to serve as a way for me to get my thoughts down in a tangible format so I panic a little less, and as a way to hopefully help you understand a bit more about the world of finances.

Dissecting the financial aid package

Well... mine, at least

The best way to familiarize yourself with how your scholarships are taxed is to simply look at them—with context. For the sake of simplicity, transparency, and my laziness, we'll look at mine throughout this article. The terminology in financial aid is largely universal, so what I discuss should also pertain to your financial aid package. Below is my MIT financial aid package for school year 2025-2026.

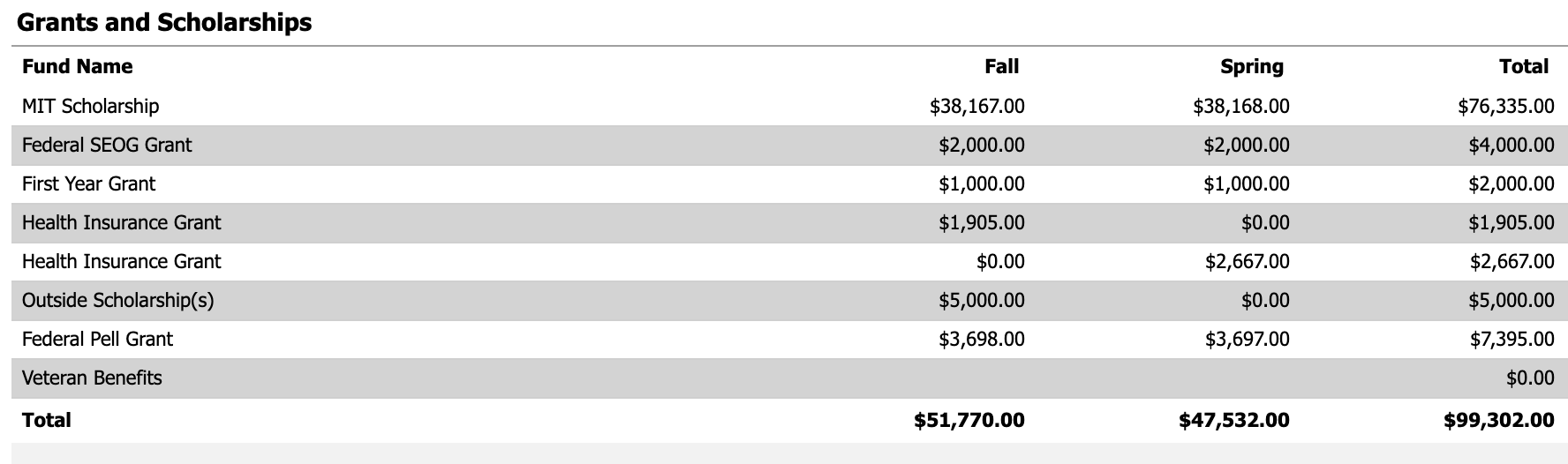

At first, it may look a bit confusing—but it's overall pretty simple. The first image—"Grants and Scholarships"—shows the specific funds that are funding my education. For the 2025-2026 award year, I receive an institutional (MIT) scholarship in the amount of $76,335, a Federal SEOG (Supplemental Educational Opportunity Grant) in the amount of $4,000, MIT's First Year Grant of $2,000, a Health Insurance Grant of $4,572, the Federal Pell Grant of $7,395, and a local outside scholarship of $5,000. This all comes out to a total of $99,302.

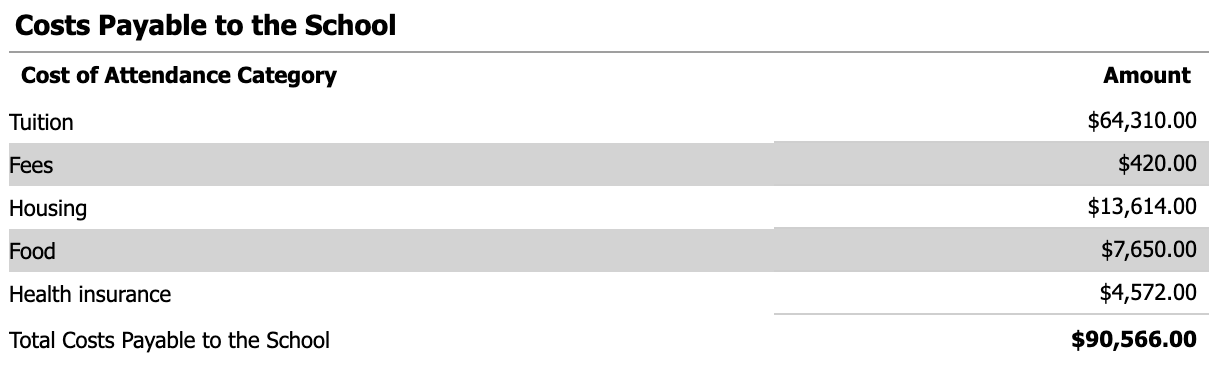

The second image—"Costs Payable to the School"—just showcases how much money is going to be paid to the school, and for what purpose; in my case, all of this is paid from my scholarships/grants. For the purposes of calculating our tax liability, scholarships and grants are effectively treated as equivalent to one another. You can see that $64,310 is going toward tuition, $420 toward required fees, $13,614 toward housing, $7,650 toward food, and $4,572 toward health insurance. This yields a total of $90,566 payable to MIT.

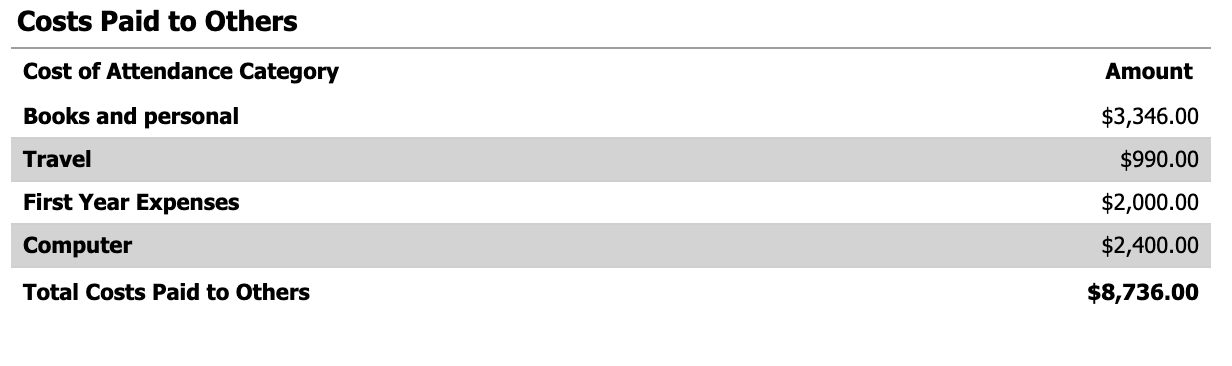

The third image—"Costs Payable to Others"—refers to the part of your Cost of Attendance that isn't necessarily paid directly to the school, but still are seen as necessary/recommended expenses for you to be able to attend college. Usually, these funds will be paid by you personally to other people—and if you have scholarships which cover these amounts (as I do), you will receive a refund from your school directly into your bank account. It lists $3,346 for "Books and personal", $990 for travel, $2,000 for first-year expenses, and $2,400 for a computer, totaling $8,736 in costs paid to others.

It is largely irrelevant in the context of tax liability whether or not you receive a refund—and if so, its amount. What we need to focus on is the specific categories of your Cost of Attendance, and your amount of scholarships to determine tax liability. I'll take a detour to the IRS to explain why.

Looking at IRS' Pub. 970 (2024), Section 1, the IRS states:

A scholarship or fellowship grant is tax free (excludable from gross income) only if you are a candidate for a degree at an eligible educational institution.

A scholarship or fellowship grant is tax free only to the extent:

1. It doesn't exceed your qualified education expenses;

2. It isn't designated or earmarked for other purposes (such as room and board), and doesn't require (by its terms) that it can't be used for qualified education expenses; and

3. It doesn't represent payment for teaching, research, or other services required as a condition for receiving the scholarship. For exceptions, see Payment for services, later.

What this means, from a simple perspective, is that you must be working toward a degree at an eligible school (which, is true) to exempt any scholarship from income (i.e. consider a scholarship tax-free), and that that tax-exempt status only applies to parts of a scholarship which don't violate 1, 2, or 3. For our purposes, number 1 is what we'll have to be cautious of; number 2 essentially reiterates number 1 other than in niche scenarios, and number 3 doesn't typically apply to undergraduate students, nor those receiving need-based aid.

So, then, looking at number 1, we can see that it stipulates that a scholarship is only tax-exempt to the point that it doesn't exceed your "qualified educational expenses". After that point, the rest of the scholarship/your scholarships are considered taxable, as they (or, at least the overage) shed their tax-exempt status. Many people get confused and assume that all of your Cost of Attendance expenses are qualified educational expenses—but that's a large miscalculation. According to the IRS in Pub. 970, qualified educational expenses for the purpose of scholarship tax liability are:

• Tuition and fees required to enroll at or attend an eligible educational institution; and

• Course-related expenses, such as fees, books, supplies, and equipment that are required for the courses at the eligible educational institution. These items must be required of all students in your course of instruction.

The IRS clarifies that the following explicitly do not qualify as qualified educational expenses:

• Room and board,

• Travel,

• Research,

• Clerical help, or

• Equipment and other expenses that aren't required for enrollment in or attendance at an eligible educational institution.

Using these definitions, we now have enough information to calculate what portion of your scholarships are considered taxable. First, look at your amount of total scholarships/grants: for me, that's $99,302 as stated previously. We'll then subtract our qualified educational expenses, using our Cost of Attendance as a base starting point. Keep in mind, your Cost of Attendance is not exact—it serves as a sort of "standard deduction", but if you feel you spent over the Cost of Attendance categories on qualified educational expenses, you can itemize your expenses and deduct them that way. Just ensure that you have proof of those expenses if you'd like to take that route—though I find the Cost of Attendance baseline as a simpler method.

Looking at my Cost of Attendance, there are several categories that I can deduct:

• Tuition ($64,310)

• Required Fees ($420)

• Books ($1,115)

• Health Insurance ($4,572)

• Computer ($2,700)

That comes out to a total of $73,117 of qualified educational expenses. You may have noticed that the number I put for Books differs from my Cost of Attendance category, as that also included "Personal". Thus, I just divided that number by 3 to get an estimate for books by themselves. Additionally, notice that Health Insurance is not typically seen as an educational expense. However, since the state of Massachusetts requires all college students enrolled 75% to full-time to have health insurance, and thus me, it qualifies as it is a "fee" that is required to attend my institution. Finally, see that despite the fact that my Cost of Attendance has a computer listed at $2,400, I listed my computer expense at $2,700. This is because I spent over that allotment on my computer, and have proof of that expense. A computer is also considered a qualified educational expense as it is a required item for my coursework (and likely most).

As you may have noticed, many important and expensive things such as housing, food, and other very real expenses are not qualified educational expenses, and thus work to increase your tax liability without being widely discussed.

Subtracting my qualified education expenses of $73,117 from my total scholarships of $99,302, we find that my total taxable income from my scholarships (or taxable scholarship amount) is $26,185. This amount is key to determining the final tax liability stemming from your scholarships.

Finding your tax liability from scholarships

Don't you love the IRS?

Keeping that aforementioned amount in mind, we now have to further dive into tax law. Typically, you would think the process would be straight forward. You determined the amount that is considered taxable income from your scholarships, and could simply list that amount on your 1040 when you file, take your standard deduction, and call it a day. But it's not. Enter Form 8615, Tax for Certain Children Who Have Unearned Income, aka the "Kiddie Tax".

According to the IRS' 2024 Instructions for Form 8615, taxable scholarships are considered "unearned income", thus invoking Form 8615.

Unearned income is generally all income other than salaries, wages, and other amounts received as pay for work actually performed (earned income). It includes taxable interest, dividends, capital gains (including capital gain distributions), rents, royalties, pension and annuity income, taxable scholarship and fellowship grants not reported on Form W-2, unemployment compensation, alimony, the taxable part of social security and pension payments, and income (other than earned income) received as the beneficiary of a trust.

The specifics of who must file Form 8615, according to the IRS, are that:

Form 8615 must be filed for any child who meets all of the following conditions.

1. The child had more than $2,600 of unearned income.

2. The child is required to file a tax return.

3. The child either:

a. Was under age 18 at the end of 2024,

b. Was age 18 at the end of 2024 and didn’t have earned income that was more than half of the child's support, or

c. Was a full-time student at least age 19 and under age 24 at the end of 2024 and didn’t have earned income that was more than half of the child's support. (Earned income is defined later. Support is defined below.)

4. At least one of the child's parents was alive at the end of 2024.

5. The child doesn’t file a joint return for 2024.

Essentially, you must file Form 8615 if your number earlier (taxable scholarship amount) was larger than $2,600 (1), you are required to file a tax return (highly likely, 2), are under 24 years old and don't provide more than half of your own support via working (3c), have at least one alive parent (4), and aren't jointly filed/married (5). If any one of those criteria doesn't apply to you however, than you can disregard Form 8615 and simply list the number calculated earlier (taxable scholarship) on your 1040. It should be also noted that dependent status is irrelevant to meet the criteria, as said by the IRS:

These rules apply whether or not the child is a dependent.

Most people likely fall under the criteria, and would have to file Form 8615 if they receive hefty scholarships. While there are some ways to potentially avoid this, as I'll discuss later, I'll continue to calculate my tax liability if I was considered to have to file Form 8615. To summarize, Form 8615 (The Kiddie Tax) will essentially take your unearned income (taxable scholarship in this instance) over a threshold ($2,600 for tax year 2024) and tax it not at your own, (probably) low marginal tax rate, but at your parent's tax rate. To demonstrate this in detail and explain the calculation of each part of the form, let's file Form 8615.

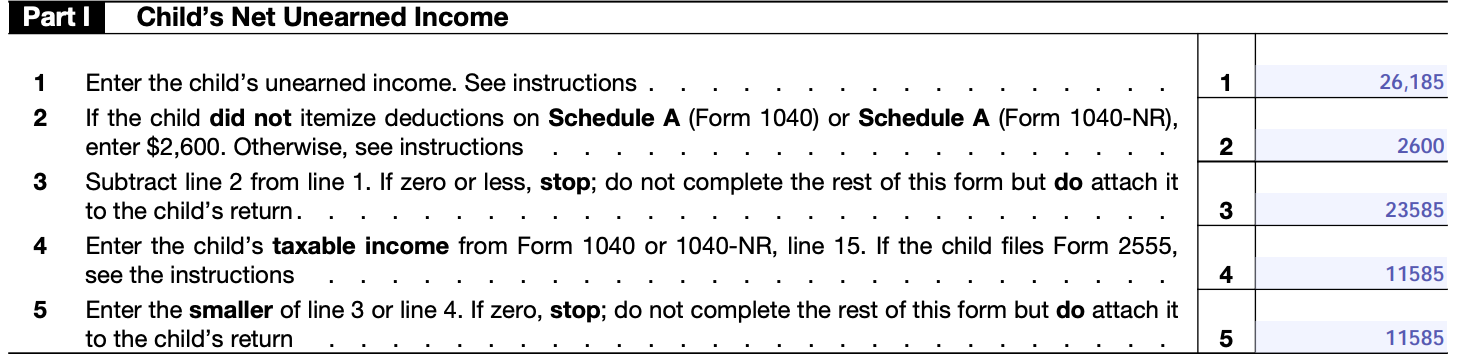

Looking at Part I of Form 8615, I entered my taxable scholarship amount (unearned income—$26,185) in box 1. Since I didn't itemize my deductions, and intended to take the standard deduction (which you likely should as well), I put $2,600 as directed in box 2. I then subtracted line 2 from line 1 and put that into box 3, yielding $23,585. To calculate box 4, you have to take a deeper dive into IRS tax law, as it requests your taxable income.

To calculate your taxable income, you essentially take your gross income and subtract your standard deduction and any other applicable deductions. You likely don't have any other applicable deductions other than your standard, and if you did you would likely know (self-employed, etc). For the sake of simplicity, this likely is satisfied by taking your taxable scholarship amount (box 1, my $26,185) and subtracting your standard deduction. It should be noted that, if you work/receive other income, you would include that with your taxable scholarship amount if you were to actually file Form 8615—however, for the purposes of this investigation we're just trying to find the tax liability generated solely from scholarships, not an estimate of your total tax liability.

Assuming you're reported as a dependent on your parent's taxes (you likely are if you're filing Form 8615), there is a more complex calculation for your standard deduction. As found in Pub. 501 (2024), the standard deduction for a dependent is calculated by:

The standard deduction for an individual who can be claimed as a dependent on another person's tax return is generally limited to the greater of:

1. $1,300, or

2. The individual's earned income for the year plus $450 (but not more than the regular standard deduction amount, generally $14,600).

Earned income defined.

Earned income is salaries, wages, tips, professional fees, and other amounts received as pay for work you actually perform.

For purposes of the standard deduction, earned income also includes any part of a taxable scholarship or fellowship grant. See chapter 1 of Pub. 970 for more information on what qualifies as a scholarship or fellowship grant.

As for the purposes of calculating this, taxable scholarship is considered earned income, you can add $450 to your previously calculated taxable scholarship. If you had any other earned income, you would add the two and then add $450. To calculate for the sake of finding tax liability linked to my scholarships, I'll add $450 to only my taxable scholarship, thus yielding $26,635. Since it's over $14,600, we "max out" — thus my standard deduction is $14,600.

Subtracting my standard deduction from my gross income (taxable scholarship) yielded $11,585, which I entered into box 4. I then entered the same amount into box 5, as it was the smaller of box 4 and box 3.

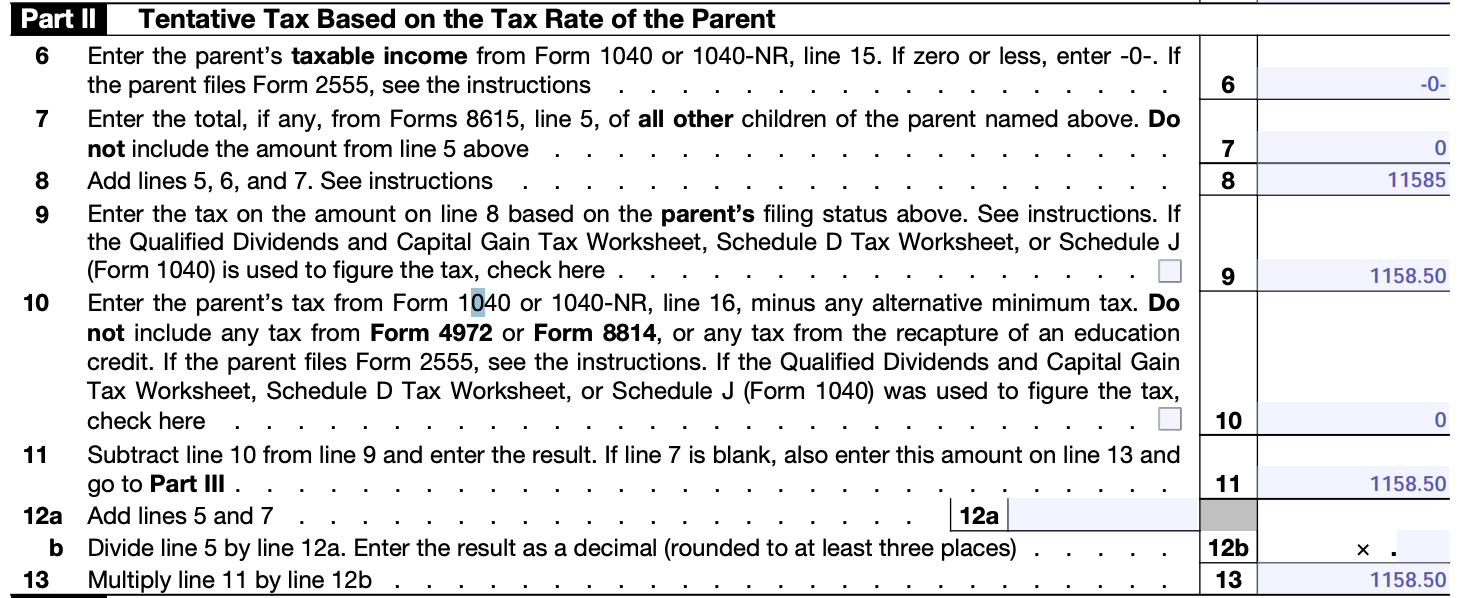

Looking at Part II, I put 0 in box 6 as my custodial parent's taxable income was 0 on their most recent 1040. I don't have any other sibling which files 8615, so I also put 0 in box 7. I added 5, 6, and 7 and put that into 8, yielding $11,585. I then looked at my parent's filing status (Head of Household) and cross-referenced that with the tax brackets. You essentially act as if box 8 was added to your parents income—thus, I added 11585 to 0, which all fell within the 10% marginal tax rate, thus I entered 10% of $11,585 into box 9 ($1158.50).

As my mom had 0 in her Form 1040's line 16, I put 0 for box 10. Thus, I yielded $1158.50 again for box 11 as I subtracted nothing. Since line 7 was blank, I followed the instructions, entered that amount ($1158.50) on line 13 and went to part III.

Part III is the last part of Form 8615, and determines how much tax liability you have. Following the titular instructions, I entered 0 on line 15 and went to line 16 as lines 4 and 5 were equal. Box 13 and 15 just added to $1158.50, which I put in box 16. Since I am a single filer, I looked at the bracket for myself in regards to box 17, and found that my entire scholarship would again be taxed at 10% (although, barely), so I entered the same $1158.50 figure in box 17. Finally, box 18 determines your final total tax owed—since line 16 and 17 were equivalent, I put $1158.50 in box 18, thus my total tax liability stemming from my scholarships is tentatively $1158.50. This is the amount you would likely have to pay in the ballpark of by the time tax season comes, if you've been following along, assuming 2024 rules are largely the same as 2025.

If you're a full-need student with a similar situation as me, particularly going to a very generous school such as MIT, then it's likely your tax burden would be close to mine. Thus, I would recommend that full-need students keep $1-1.5K untouched for taxes based on the results of this investigation, depending on your family circumstances. But, there are other things to consider as well.

Ways to potentially lower taxes owed

Rich people do it, why can't you? Right..?

There are some ways to potentially lower your taxes owed, but some come with their own disadvantages, and may not even be a benefit in your situation—or for many people.

On the 1098-T

It should be noted that the form that colleges use to report financial information about students, Form 1098-T, is rumored to not be incorporated into the IRS' Automated Underreporter system. This means that the IRS does not typically corroborate this information with tax returns, and the risk of being audited for failing to report taxable scholarship has historically been low. However, I do not recommend doing your taxes based on purposeful ignorance—tax debt is a real thing, and has been a large issue in my own family. The key to financial stability is to be aware and knowledgable on these topics and use that to be responsible. There is always the possibility that the IRS will change its policy and start to rampantly utilize the 1098-T to detect tax underreporting, and thus the sensible option is to obey the law while doing the best you can to reduce your liability. Additionally, you may lose out on potential educational tax credits (such as those mentioned below) if you ignore your 1098-T, which could be result in a net positive despite increased tax liability.

American Opportunity Tax Credit

The American Opportunity Tax Credit (AOTC) is essentially intended for undergraduate students who meet a broad set of criteria; it is a partially-refundable tax credit, which means it can result in a tax refund (and thus money given back to you from the government). There is a maximum yearly credit of $2,500 per student, and 40% (up to $1,000) is refundable after tax liability is reduced to 0. It can be claimed by you, or your parent if you are claimed as a dependent, but not both. The credit is calculated as 100% of the first $2,000 of qualified educational expenses (as we defined earlier) and then 25% of the next $2,000 of qualified educational expenses paid in a non-tax-exempt manner. This means that you would have to decrease the amount of qualified educational expenses we subtracted from the total scholarship amount previously, bringing up your taxable scholarship (unearned income) but simultaneously making you eligible for a more advantageous tax credit that will often outweigh the increase in taxable scholarship by a lot.

Lifetime Learning Credit

The Lifetime Learning Credit (LLC) is a much broader educational credit: it is simply intended for students enrolled in some manner of eligible higher education. There is a maximum yearly credit of $2,000 per return, and it is non-refundable. The credit is calculated as 20% of the first $10,000 you pay in qualified educational expenses. It can be claimed by you, or your parent if you are claimed as a dependent, but not both.

Earned Income Tax Credit

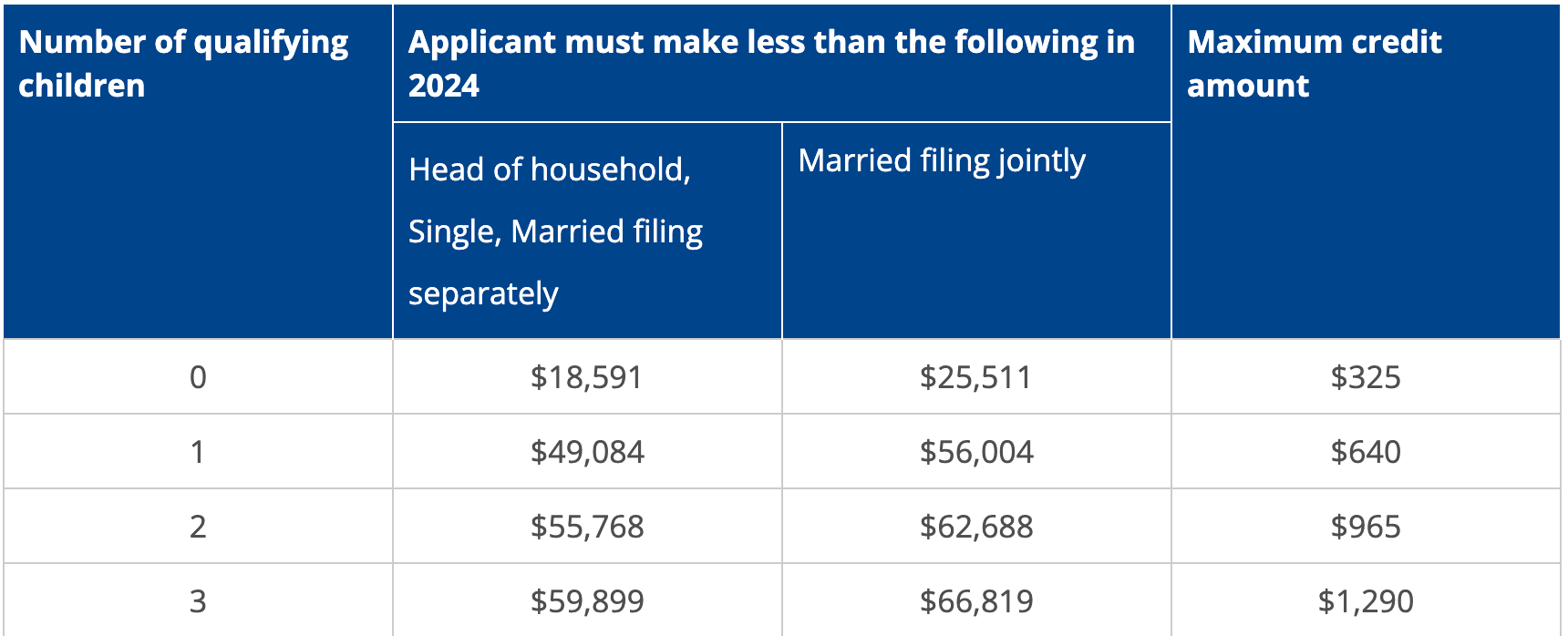

The Earned Income Tax Credit (EITC) is primarily aimed at lower income families, aiming to provide tangible refundable tax relief to those who need it. It is heavily skewed toward low-income families, and particularly larger ones, as seen on the credit amounts as listed:

The maximum amount of credit:

• No qualifying children: $632

• 1 qualifying child: $4,213

• 2 qualifying children: $6,960

• 3 or more qualifying children: $7,830

This is not something directly applicable to your educational tax burden, but it is key to consider for students from low-income families before they attempt to become independent for tax purposes, as it could lead to the loss of a large amount of tangible funds for your family. Below is the income qualification bracket for the EITC—if your family doesn't fit solidly within those barriers, then considering the EITC may be a null point when considering independence for tax purposes.

Independence for Tax Purposes

Another option to consider is to avoid the Kiddie Tax (Form 8615) by not fulfilling all of its criteria. The most easy part of the criteria to avoid is to essentially become independent for tax purposes—that is, you must provide more than half of your own support via earned income (from a job/work). However, this comes with a trade-off. At that point, your parents will no longer be able to claim you as a dependent on their taxes. For many low-income families, this is a significant blow which overpowers the student's personal tax burden savings.

For example, in my case, if I were to be independent for the sake of taxes by working to provide half my support, I would be able to claim the AOTC. That would reduce my taxes owed to $0, and give me a refund of $1,000 if I optimized my taxable scholarship and qualified educational expenses distribution. But, I'd have no use for the LLC, as I wouldn't make enough to have a use for it as a college student after the AOTC. Additionally, it would remove my parent from being able to claim the EITC for me—as I have one dependent sibling, that would represent a loss of up to $2,747 for my parent, and up to $3,581 if I were an only child. If I had two dependent siblings, however, then it would represent a loss of up to $870. This is assuming your parent is claiming the maximum EITC by optimizing their tax return.

Thus, while I would go from owing $1,158 to getting a refund of $1,000, my parent would lose $2,747, which means there's a net loss of $589. If I were to stay a dependent, my parent would be able to claim the AOTC and EITC, garnering $3,747 in total, though I would still have my tax burden of $1,158. Still, that's a net positive of $2,589.

This will look different for every family, but most low-income ones will likely be better off overall if students stay as dependents. An exception to this would be if there are already 2+ dependent children being claimed apart from you.

Middle-income families will have to weigh this in a more precarious state. While the AOTC and LLC may be helpful, depending on your parent's marginal tax rate, it may be better to strive for independence. Additionally, higher-income families will have to consider ineligibility for the AOTC and LLC. This can make it easier to see the benefit of attempting to be independent for tax purposes, but it may be much more difficult as your parent likely provides an amount of support that cannot be supplanted by your own earned income.

My own choice

With all this research in mind, coming from a poor family, I will probably elect to continue being a dependent for tax purposes and eat the personal tax burden in order to have a net positive outcome for my family. This is also further exacerbated as my state of residency (Washington) offers the Washington Working Families Tax Credit, of which dependent children (defined by the same criteria for the aforementioned EITC) is also a consideration. If I were to lose my dependent status, it would likely cost my family another $325, which further demonstrates that staying a dependent will result in the best outcome for my family.

TL;DR

Don't worry, it was a long read

- Scholarships are tax-exempt when used for tuition and required fees, supplies or equipment

- Scholarships are taxable when used for food, housing, personal expenses, and other non-qualified educational expenses

- Staying a dependent will likely benefit you and your family's tax liability overall, particularly for low-income families

- If you're under 24, are claimed as a dependent, and have more than $2,600 in taxable scholarships, you likely have to deal with the Kiddie Tax (Form 8615)

If you didn't bother to read that all, I can't blame you—but I think it's worth it. Regardless, if you are on full-aid or have significant scholarships past tuition, save $800-$1,500 for potential tax liability come tax season as a relatively conservative estimate. While there may be ways to optimize your tax liability, as I discussed, it differs for each family, person, and situation—do the financially responsible thing and save so that you don't get stuck in a hard situation.

While I am not a professional CPA by any stretch of the imagination (though I find taxes fun and maybe you'll find me at a VITA soon), I hope that I was able to give you a scoop into the world of taxes and Uncle Sam in a digestible way. This sort of understanding is definitely something I could've used before I went on my manhunt for research into such a barren desert of knowledge.